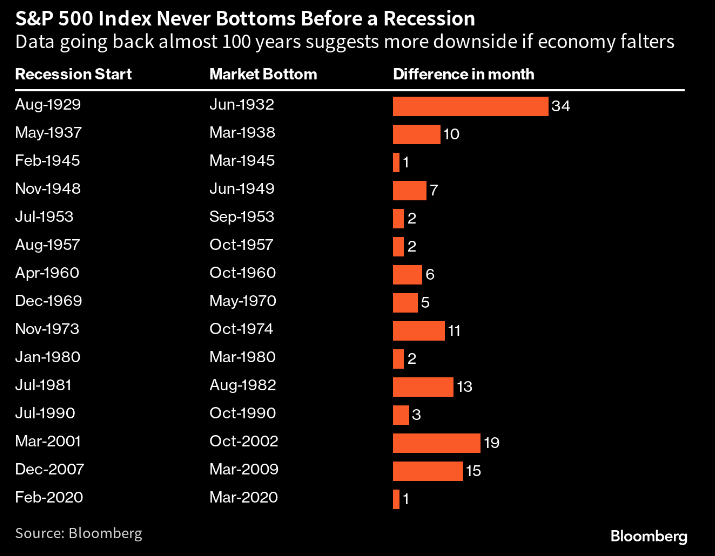

That’s what BBG is serving up this morning, explaining that US markets have never bottomed before a recession, in the roughly 100 year data set they track, so bulls are forewarned. Previous lows are now -15% down from current levels. CS gives an 80% probability that the US enters a recession by 1Q24.

That’s what BBG is serving up this morning, explaining that US markets have never bottomed before a recession, in the roughly 100 year data set they track, so bulls are forewarned. Previous lows are now -15% down from current levels. CS gives an 80% probability that the US enters a recession by 1Q24.

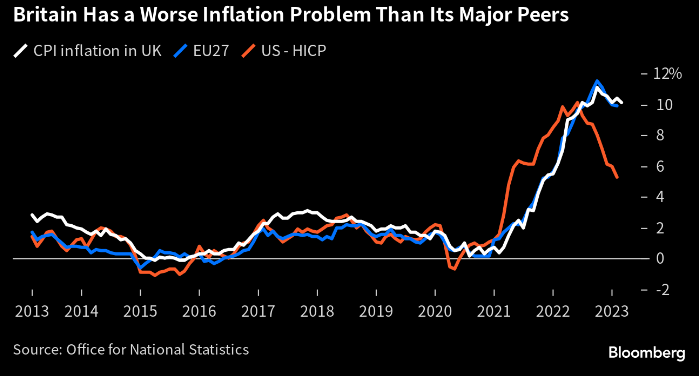

That’s what the inflation print out of the UK read this morning, with the CPI up 10%+ y/y in March driven by the hottest increase in food prices in 4 decades. Of course investors quickly priced in more rate hikes from the BOE. Because of high energy prices and workforce ghosts, the UK basically combines the most challenging aspects of the EZ and the US.

We’ve started hearing from the regionals. Bancorp had a rise in deposits. Citizens Financial cut FY23 guidance and reported lower deposits. Net income for Morgan Stanley was down -20% because of lower trading and investment banking, and provisions for credit losses were 4x y/y at $234mm due to commercial real estate and a worsening economy.

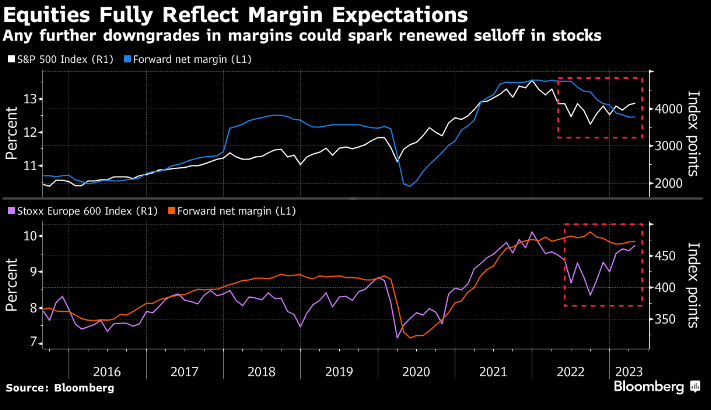

That’s what Teslas are doing, with Musk cutting prices (again) on some models ahead of 1Q23 results later today. The Model Y SUV is down -$3k, and the base Model 3 now is under $40k. As you know, if you cut prices, you cut margins. BBG data shows that equities are expecting margin pressure, especially in the US, but if we keep seeing lower prices/margins, then equities have more room to fall.

Various Fed folks are out, talking about rates. But the benchmark here in the US sits between 4.75-5.0%. Swaps are only pricing in a 25bps hike in May, and then they assume rate cuts start in July. To get the Fed to not just pause but reverse course, in our opinion, the economy would have to absolutely tank in a short-term horizon, which we’re just not buying. So, we would expect markets to push out any dovish moves until 2H23 or 1H24, which could hurt duration assets.

The $787.5mm settlement by Fox to Dominion (about half of the damage demand) is a big recovery in any lawsuit, according to experts. Staple Street Capital, who paid $38.3mm to acquire 76% of the co in 2018, was the biggest winner of the decision.

Although Netflix shares are down because of fewer subscriber adds, the company raised its FY23 free cash flow forecast. We don’t mind a company kicking out freeloaders while increasing cash flow in a challenging economic environment. It will give them optionality to grow paying subscriber numbers in the long haul and invest in its business.

CDW is down hard after missing rev estimates. This is a company that reflects corporate spend—and its numbers are telling you that companies aren’t loose with their pocketbooks right now, especially the big ones. Remember our note on Google and sharing staplers? Also, Ally Financials’ profit fell more than expected because it made fewer loans and raised its default provisions. Customers are falling behind on car payments at rates that rival 2009. For all the talk about higher savings levels boosting US GDP, keep this nugget in mind, folks.

That’s what Bard seems to be. Google’s AI chatbot, according to internal employees, was released too soon. A “pathological liar” that was released to “keep up with the Joneses” seems to be reflective of everyone under the sun claiming AI features. It must hurt that the OG (MSFT) released OpenAI first. With the ratio of (a) techies building AI to (b) those focused on AI safety at 30-to-1, per the Center for Human Tech, users should be careful.

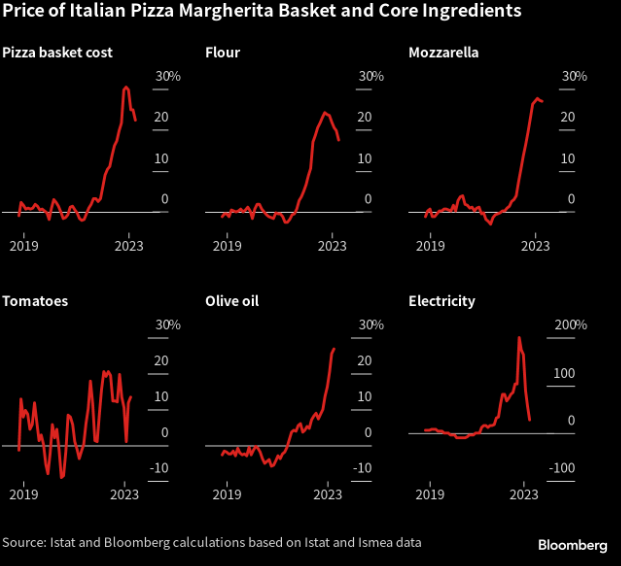

BBG reports that its proprietary Bloomberg Pizza Margherita Index is flashing red as it is now over 20% more expensive to make a pizza at home than a year ago. The rise is driven primarily by an unrelenting increase in the price of olive oil (up 27% y/y) reflecting reduced supply out of Spain due to a devastating drought. Meanwhile, Heineken reported better-than-feared results that showed that Europeans are still buying its beer despite the higher prices. Management noted that results performed “ahead of our expectations as consumers remain resilient so far despite continued pressure from inflation across consumer goods.” Perhaps they are just switching to a liquid diet…