Applications for jobless benefits rose to their highest level in >1yr (+11k to 239k w/w), but they’re still are low levels on an absolute basis. Roughly 1.81mm people received jobless benefits for the week ending April 1, a figure down -13k from the prior week—and at a level close to pre-pandemic levels. Also, producer prices came in at +2.7% y/y vs an expected 3%, so the market is up (for now).

Applications for jobless benefits rose to their highest level in >1yr (+11k to 239k w/w), but they’re still are low levels on an absolute basis. Roughly 1.81mm people received jobless benefits for the week ending April 1, a figure down -13k from the prior week—and at a level close to pre-pandemic levels. Also, producer prices came in at +2.7% y/y vs an expected 3%, so the market is up (for now).

Part of the strength in US equities this year has come from buybacks and LBOs. JPM also is out with a note explaining how unlevered and levered investors are fairly neutrally positioned—but while that positioning could limit downside, it wouldn’t prevent a correction. Also, JPM noted that US money market inflows slowed through Easter to $24bn, but we caution that people could have just been busy—so we’ll be watching for future data points.

Get ready for banking banter tomorrow, with some biggies printing earnings such as $JPM $C $WFC and $PNC. The Q&A will be really interesting, not just from a deposit perspective but also from a regulatory one. Will they talk about the likelihood for regulation on higher liquidity levels, capital charges levied against excessive levels of uninsured deposits, AOCI (Accumulated Other Comprehensive Income) amounts being included in regulatory capital, and other initiatives that will pressure margins? Probably not, but smart analysts will be asking hopefully, because it’s not what they printed for this quarter, but what’s ahead.

A survey by the Intl Assoc of Credit Portfolio Managers points to more corporate defaults this year: 86% expect them in the US, and 84% expect a recession. Roughly 60% expect credit spreads to widen in the next 3 mo (when riskier debt is forced to offer yields much higher than less risky debt).

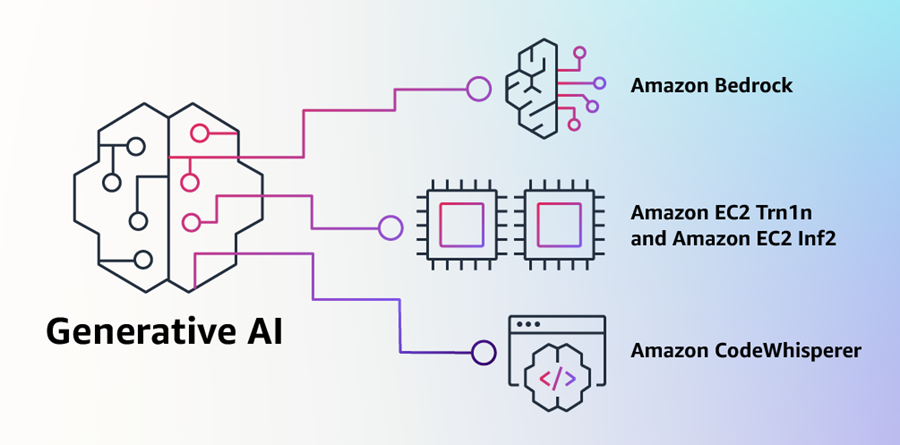

Not to be outdone, $AMZN is launching Bedrock, a new cloud service and suite of proprietary language models. Basically, clients can use language models from Amazon (called Titan), AI21, Anthropic and Stability AI. First clients will be Pegasystems, Deloitte and Accenture. Following $MSFT and $GOOG announcements, we would expect nothing less. Supposedly they have been working on this for decades, and AWS has >100k AI customers.

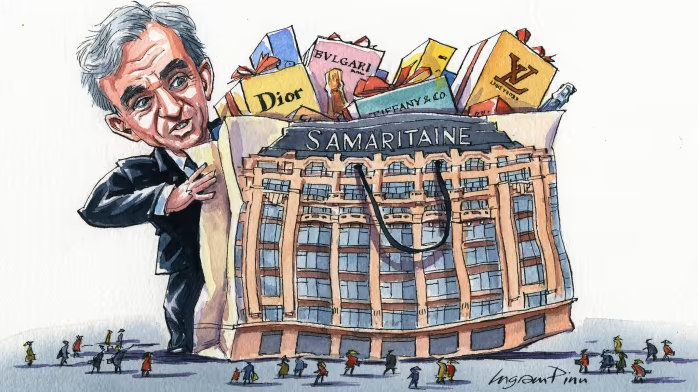

LVMH had a big beat on earnings, showing how it’s done. Commentary, though, is interesting to note. The US is getting softer. The Chinese consumer is recovering according to expectations, but not at the levels of major bulls. Dior was strong. Wine and Spirits were solid because of champagne. Sephora was strong in the US. Perfume, cosmetics, watches and jewelry also were above expectations. What is the read across to other companies? Probably good for large companies with strong brands that have invested in stores and online. But not so good for less-solid brands or for companies who don’t have a huge platform.

It seems like a lot of countries are getting together to isolate the 2 biggies on the block. Macron is in hot water for his buddy-buddy comments supporting China and isolating the US and Taiwan. Remember our note about Brazil’s new deal to be able to pay in yuan vs dollars? Also, the Saudi-Russian oil alliance could keep oil >$80/barrel and continue to weaken US’ power. Plus, companies have successfully been shifting production away from China. Apple tripled its India iPhone production to $7bn last FY. The US purchased computer chip machines at a record level in March (+43% y/y to $71.3bn). What to make of all of this? It is inflationary. Plus, it heightens geopolitical risks for investors.

Today a new feature on Twitter is being rolled out, whereby users can view financial charts on more instruments and also use eToro to trade stocks and other assets. Users could click a “cashtag” (a dollar sign followed by a ticker) to access new features.

I know it can be tough to keep track of rate cycles around the world, so in a nutshell:

1. the recent US Fed minutes reiterate a need to keep data-focused but also flexible with policy, so expect 25bps hike at the next meeting and then the inflation and labor data to REALLY matter for future hikes.

2. In the EZ, they’ll do another 25bps hike in May—and if inflation stays high and sticky, they could keep raising and narrow the gap with US rate levels.

3. In Japan, the BOJ is still on yield control, so don’t expect much action right now.

4. Singapore may tighten tomorrow—it’s a bit of a toss-up.

The price of crypto ether reached >$2k for the 1st time in 8 mo post Shanghai upgrade. Ethereum staking withdrawals were enabled after a 2-yr lockup period. Investors appear relieved at the relatively calm price action so far, given concerns what the added liquidity would do.