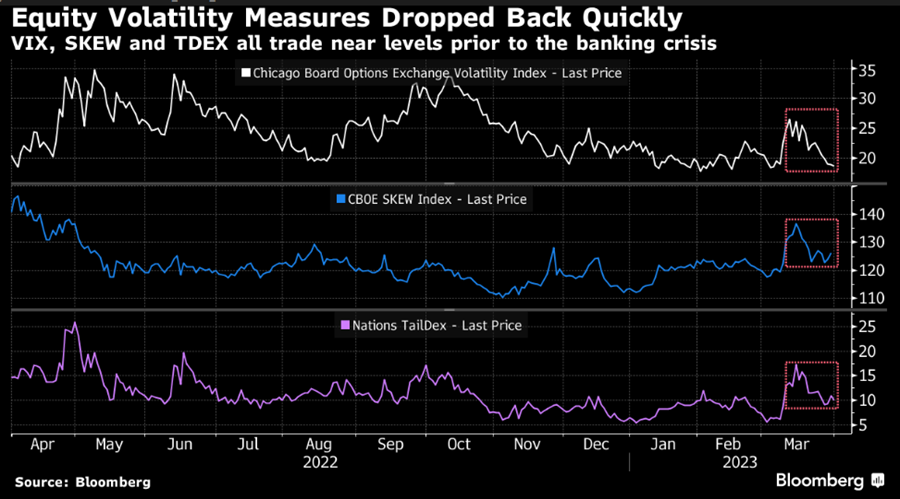

Versus bonds, equities are showing low vol, with the VIX below 20. In fact, volatility has dropped back to pre-banking crisis levels. With growth pressures, high labor costs, and financing costs/availability challenged, it seems a bit optimistic to be complacent before earnings season begins in a couple of weeks.

Versus bonds, equities are showing low vol, with the VIX below 20. In fact, volatility has dropped back to pre-banking crisis levels. With growth pressures, high labor costs, and financing costs/availability challenged, it seems a bit optimistic to be complacent before earnings season begins in a couple of weeks.

US Factory activity is down more than expected, to the lowest level since May 2020. Excluding the pandemic, the 46.3 reading was the worst since 2009. Which is never a good comparison year. Also, headcount declined. Inventories shrunk. Priced paid for materials reflected a decline in costs, which is good in terms of fighting inflation.

The MOVE Index, which tracks treasury volatility, is still high, pointing to uncertainty in the path of interest rates here in the US.

Treasury yields jumped because of crude oil’s rally. OPEC made a surprise 1mm barrel oil production cut after previously assuring partners it would hold supply steady to maintain stability in the market. Want to know what could upend the recent equity rally? Higher inflation from higher energy costs. Saudi Arabia announced a 500k barrel/day reduction. Then Kuwait, the UAE and Algeria followed.

Tesla deliveries (422k cars) are at a record after reducing prices. The most sales were from the Model 3 sedan and the Y crossover.

That’s what 20-30% of UBS’ workforce will be up to (~36k jobs globally lost) post CS merger. Around 30% of the companies’ workforce were in Switzerland alone, so roughly 11k of the cuts will happen there. Know who’s excited? Bain, BCG, McKinsey and Oliver Wyman are all bidding on what should be a lucrative gig assisting with the transition.

Asia’s growth seems to be slowing. South Korean exports are down. Japan’s Tankan survey of large manufacturers declined to a 2-year low. China’s Caixin manufacturing PMI fell to 50 in March (remember, below 50 is a contraction).

Or any other mph, for that matter, if the cost of auto loan rates stay this high. Current financing rates are at 7-8%, which is separate from higher vehicle costs. Per Cox Automotive, with an ave car price of $50k, an auto loan payment is now $784/mo, up $177/mo since the Mar 2020 pandemic crunch. BBG is out with a story talking about how buyers are cancelling orders for hard-to-get models that they signed up for months ago. They ordered the car when the rate was 2%, and now it’s 8%.

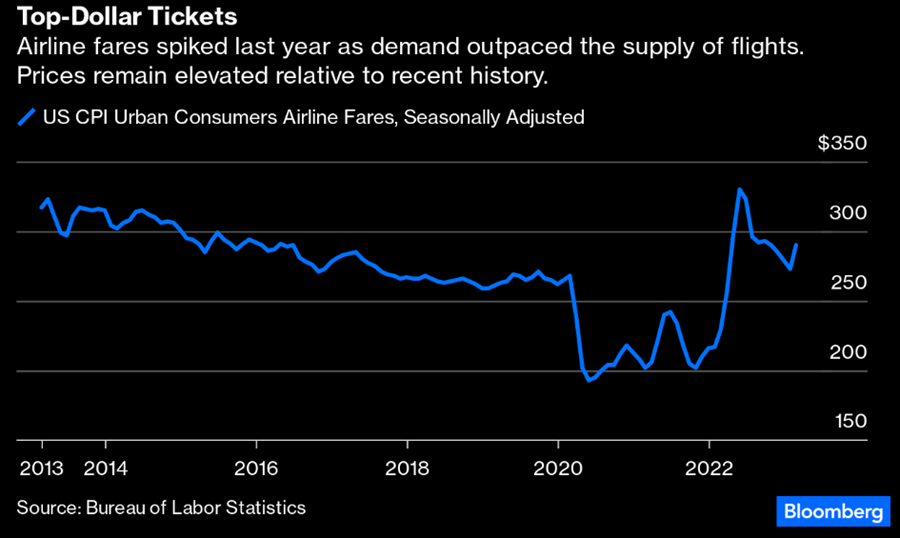

Analysts are expecting another crazy summer of travel. So, expect delays, cancellations, long lines, lost baggage, and other fun times this summer. Travelers are not scared off, though, and are keeping prices high due to demand. So, I guess you can buy into airline stocks, unless the gas price increase gets too high.

Or at least it seems that Pinduoduo does, with reports out that the Chinese app can bypass cell phone security (especially with Android O/S) and spy on users and competitors’ apps. This comes on the heels of learning that the Chinese spy balloon was able to gather intelligence from sensitive American military sites, despite the gov’s attempts to stop it. China was able to control the balloon so it could make multiple passes over some of the sites (sometimes flying in figure 8 formations) and transmit the info back to Beijing in real time. The intelligence was mostly from electronic signals and not images.