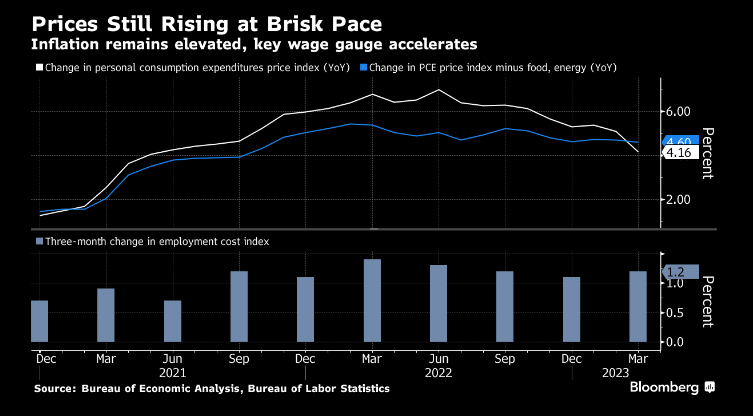

Inflation (PCE) for Mar came in at 0.3% m/m, which roughly matched expectations. So, we expect 25bps from the Fed in May, as higher inflation is not the direction they want to see. They have to find a way to get the +4.6% y/y inflation read down to their targeted 2%, so their Q&A will drive markets depending on the story given. US employment costs (benefits and wages) were up +1.2% in the quarter, above forecasts. Adjusted for prices, the detailed data is showing that consumers are pulling back a bit on discretionary purchases. There’s only so much they’ll pay for a $SBUX latte.

Inflation (PCE) for Mar came in at 0.3% m/m, which roughly matched expectations. So, we expect 25bps from the Fed in May, as higher inflation is not the direction they want to see. They have to find a way to get the +4.6% y/y inflation read down to their targeted 2%, so their Q&A will drive markets depending on the story given. US employment costs (benefits and wages) were up +1.2% in the quarter, above forecasts. Adjusted for prices, the detailed data is showing that consumers are pulling back a bit on discretionary purchases. There’s only so much they’ll pay for a $SBUX latte.

Traders pumped up $AMZN stock after-hours until they digested the earnings details. There were a lot of positives (reduced expenses and initiatives making progress such as same day, better grocery) but the growth in web services cooled to 16%, with April slowing to 11%. They are counting on AI to reverse this trend, but was a lack of AI really to blame? $INTC reported a miss on earnings but a beat of revenues, yet investors focused on a perceived profit trough as well as their tech roadmap and deal announcements to consider it an overall win post-market.

The sound of the clock countdown for $FRC is growing louder. Will the government step in? Will they find a suitor? In any case, the unknown is sure to be spurring more deposit outflows. Fun fact—the Fed balance sheet declined by ~$30bn this week, but the draw from the discount window rose ~$4bn to $73.8bn. The recent pattern has been for the discount window to decline, and the BTFP to rise as borrowings shift to the less onerous facility, so this change reflects increased pressure on regional banks in the past week.

Per UBS, US investment grade reversed from inflows to outflows, with -$1.32bn leaving compared to inflows of +$1.14bn the prior week and $+12.37bn YTD. High yield kept attracting flows, with inflows at +$593.9mm versus +$3.06bn the prior week, with $-9.39bn YTD. If we hit a credit cycle, be careful if you’re putting money in high yield.

Both Exxon $XOM and Chevron $CVX beat on revenues and earnings. $XOM is targeting $9bn in cost savings by year-end.

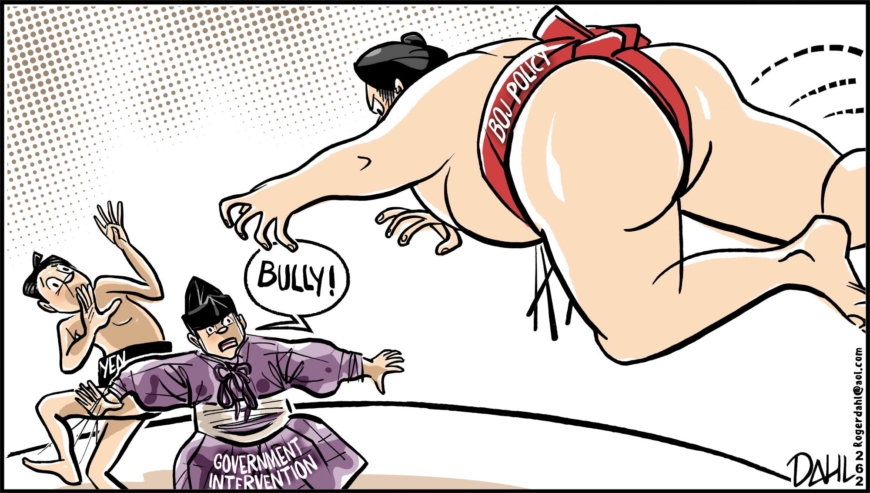

The BOJ left its main policy settings unchanged, with no change to yield curve control, but scrapped guidance on future rate levels. In response, the yen weakened sharply, equities rallied (ex banks), and JGB yields fell. Japanese data reflected Tokyo core inflation unexpectedly rebounding in April, national industrial production growth slowing, and retail sales growth above forecasts.

Tons of Eurozone data out, with a mostly mixed reading. EZ GDP up +1.3% y/y vs consensus +1.4%–so, slower growth. German GDP missed (0.1%) q/q vs consensus +0.3%, with unemployment up +24K faster than expected +10K. France GDP was in line with consensus +0.2% q/q. Italy grew faster than expected (+0.5% vs +0.2%), and so did Spain (+0.5% q/q vs +0.3%). CPI was hotter than expected in France and Spain.

The Fed is going to publish its internal review of SVB’s collapse, sure to be a best-selling summer read for the financially-oriented.

It’s summertime, and short sellers are bringing out their shorts against commercial mortgage REITS. With higher interest and lower property values (did anyone else read that frightening BBG story about the downtown SF office building?) plus continued WFH, the bet is that borrower will default. Blackstone Mortgage Trust and Starwood Property Trust both suffered post-pandemic high short levels this past month (around 14-16%), per S&P.