Day traders’ passion for zero-day options (options that expire <24 hrs) looks like a money pit. German researchers estimate they lost on ave $358k a day since May 2022, when it became possible to trade expiring contracts every day. Other analysts estimate that novice investors took a $1bn hit from options during the pandemic, so it’s not a surprise to see this newer fad not working out.

Day traders’ passion for zero-day options (options that expire <24 hrs) looks like a money pit. German researchers estimate they lost on ave $358k a day since May 2022, when it became possible to trade expiring contracts every day. Other analysts estimate that novice investors took a $1bn hit from options during the pandemic, so it’s not a surprise to see this newer fad not working out.

My colleague flagged this gem in an 8-k filed yesterday. Outside of its boosting profits via stapler access reduction (we’re still getting our arms around that one), Google is decreasing its depreciation expenses by $3.4bn by extending the useful lives of servers and network equipment to 6 years. That’s one way to increase financial statement profits…akin to financial magic. The irony is that the stapler curtailing program will have more actual cashflow benefit than this hocus pocus.

P&G is giving a big hug to shareholders this morning, raising its revenue forecasts given higher prices offsetting lower demand. Organic sales increased by +7%, yet volume declined by -3% as customers downshifted to cheaper brands. Prices were up a whopping +10% y/y. Seems like there’s elasticity for Febreez

Yesterday’s Leading Indicators index was <0 for the 12th consecutive mo and hit a new low. Ex-early pandemic days, the series had not fallen to such a low level since the GFC. The Philly Fed figure hit a trough too, adding to the batch of weak macro data that isn’t confirming the soft-landing scenario. Investors are still pricing in a 50bps rate cut by year-end, but inflation is still high. Re-read the Charmin note above. Also, today’s US business activity data hit a roughly 1-yr high, pointing to inflation staying strong. Obviously there are a lot of data points that you can choose from, here….but the key point is that they tell a divergent story, so taking strong one-way bets at this point may be premature.

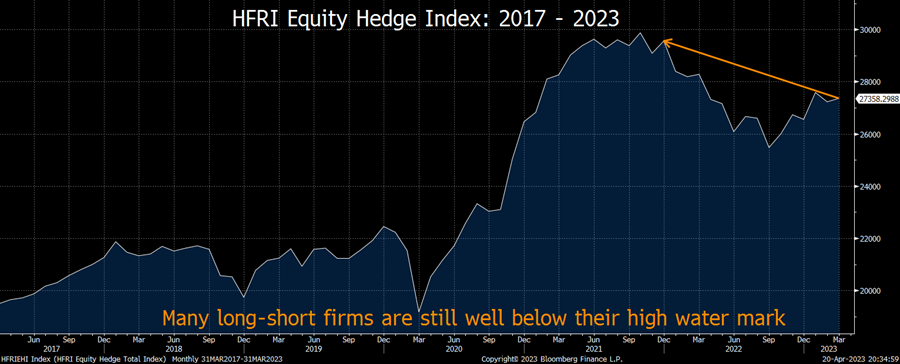

Because the ave L/S hedge fund only captured 25% of the March gain for the S&P 500, UBS puts out a good note explaining why they have an incentive to buy the dips during these final days in April—they took off shorts, to chase the returns, and they need April to validate that move. Still below their high water mark, they need profits.

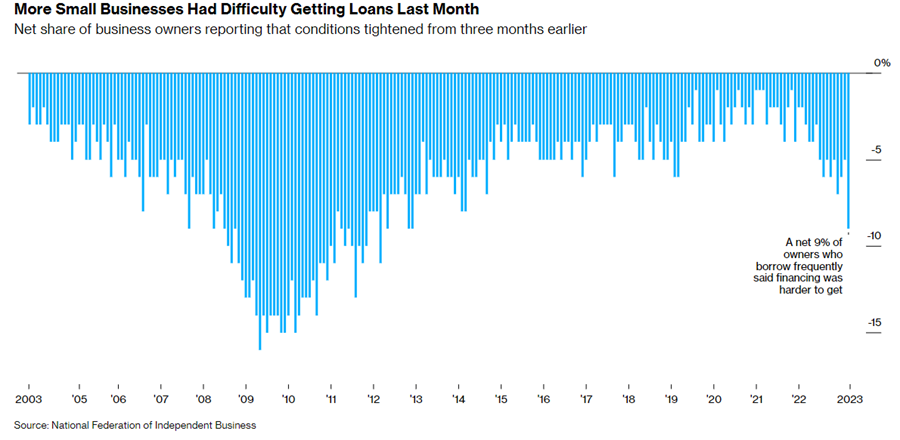

BBG is out with a story about tighter credit conditions and provided this gem chart (below). Banks are seeing the credit crunch, including bankruptcies—mostly concentrated in construction, health care and retail. A lack of credit will continue to hit SMID businesses, which are big drivers of GDP and employment here in the US. Per BBG, the volume of US corporate debt trading at distressed levels (10bps+ over the benchmark for bonds, or trading at <80 cents on the dollar for loans) increased by 28% last mo to $400bn. That compares to last year’s figure of $74bn. It is again simple math that tells a dark story here.