With Tom Cochrane’s “Life is a Highway” on the radio this morning, we’ll stay in the Auto Zone today as we head deeper into earnings season. Guidance and the Q&A from Big Tech this week will either drive equity markets higher or force analysts to keep cutting profit forecasts. Remember, right now analysts have 2024 figures up +9.9% y/y. With the macro data we share with you, alongside continued central bank tightening impacts and liquidity drain, we’ll take the opposite side of that trade. For $GOOG, we expect we’ll hear a ton about AI, but we’ll be focused on search revenue growth trends today. $META has high expectations built in, with an everyone-seems-to-own-it investor base, so unless they guide high, risk seems to be to the downside. Plus, remember the Year of Efficiency? We’ll see if it becomes the "Couple of Quarters of Efficiency” as AI overtakes the Metaverse in investors’ minds. $AMZN = AWS, and with analyst estimates continuing to decline, if the company can point to the “bottom” of growth, then I think asymmetry would be to the upside. $MSFT = Azure growth, which has been decelerating of late. No matter what the company talks up about AI, corporate spend is challenging (remember CDW’s print?).

With Tom Cochrane’s “Life is a Highway” on the radio this morning, we’ll stay in the Auto Zone today as we head deeper into earnings season. Guidance and the Q&A from Big Tech this week will either drive equity markets higher or force analysts to keep cutting profit forecasts. Remember, right now analysts have 2024 figures up +9.9% y/y. With the macro data we share with you, alongside continued central bank tightening impacts and liquidity drain, we’ll take the opposite side of that trade. For $GOOG, we expect we’ll hear a ton about AI, but we’ll be focused on search revenue growth trends today. $META has high expectations built in, with an everyone-seems-to-own-it investor base, so unless they guide high, risk seems to be to the downside. Plus, remember the Year of Efficiency? We’ll see if it becomes the "Couple of Quarters of Efficiency” as AI overtakes the Metaverse in investors’ minds. $AMZN = AWS, and with analyst estimates continuing to decline, if the company can point to the “bottom” of growth, then I think asymmetry would be to the upside. $MSFT = Azure growth, which has been decelerating of late. No matter what the company talks up about AI, corporate spend is challenging (remember CDW’s print?).

That’s what Coca-Cola is firing on—higher prices with higher demand (versus P&G’s higher prices and lower demand). So keep watching your favorite company’s earnings reports to understand the key trends that will drive future results. Demand destruction is rarely a winning strategy.

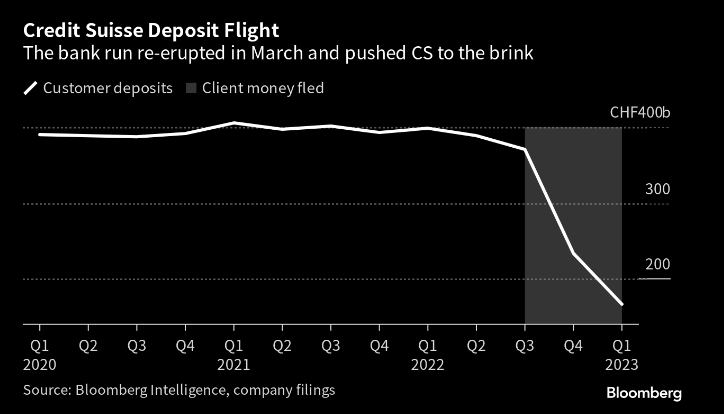

CS suffered $69bn of outflows in 1Q23 and took a major write-down in its wealth mgmt unit, driving a total loss for the past 6 mo of over $200bn. This points to the challenge UBS will have retaining key clients and employees which, during a crisis, don’t care if you’ve been in business for 167 years. Don’t feel bad for UBS, though, they paid roughly 3bn francs for a business ending March with a book value of 54bn francs while the government wiped out bondholders.

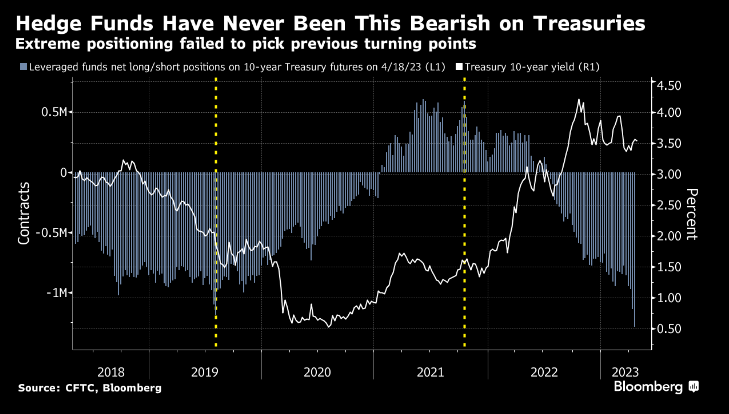

Swap markets still are pricing in Fed rate cuts this year, akin to a potential fuel injection for the market. But hedge funds are betting on the opposite and have put on a record Treasury short, betting that the Fed will have to hike rates, given a decent economy with sticky, high inflation.

VC investment in climate tech hit a record $70bn last year, per HolonIQ Global Impact Intelligence. That’s an increase y/y of 89% during a period when vc investment declined overall. With the support of public funding/backing, start-ups attempting to reduce carbon impact are hot. BBG estimates that around $650bn went to climate fixes in 2019 and 2020, with roughly half from public and half from private capital sources. Emission reductions was the big winner ($586bn), followed by adaptation measures ($49bn), per the Climate Policy Initiative. We’ll have to see how the Inflation Reduction Act spurs deployment of solar and wind power and drives improvement in carbon capture, ag, batteries, and other key areas.

![]()

That’s what I am feeling just reading the headline from the FT: “US banks on alert over falling commercial real estate valuations.” OK, they didn’t do a spreadsheet to figure out that rising rates would crush their long-duration Treasuries and bonds. Now we’re figuring out that they didn’t do a spreadsheet to figure out what would happen if commercial real estate declined post-pandemic, as most humans prefer wearing shorts and walking a few steps to suits and taking public transport.