Consensus for next week’s Core CPI print on Wed and Ave Hr Earnings is still hot, so any weakening of these metrics could continue to drive risk assets higher---giving a couple of data points for the “Fed rate hike pause” team. Tomorrow we’re getting payrolls and unemployment data, which will be digested into market action on Monday, as tomorrow is a market holiday in the US.

Consensus for next week’s Core CPI print on Wed and Ave Hr Earnings is still hot, so any weakening of these metrics could continue to drive risk assets higher---giving a couple of data points for the “Fed rate hike pause” team. Tomorrow we’re getting payrolls and unemployment data, which will be digested into market action on Monday, as tomorrow is a market holiday in the US.

HFR data points to flat returns for hedge funds in 1Q23. CFTC non-commercials maintained net shorts in UST futures and US equity index futures during the quarter, skewing the risks towards short covering near-term in Q2, unless the data becomes confirming for them.

Per 42Macro, although there have been two prior pause pivots which were bullish for markets, in those two instances they enabled investors to maintain a “soft landing” expectation for a year—a time frame that 42 Macro doesn’t believe exists today. They’re pegging it at 1-2 quarters…at most. Moreover, the Fed is looking for a downturn in labor and inflation, so the dreams of rate cuts and QE mojo are a lot less likely.

Costco’s comparable sales slowed in March, with core comps turning negative for the first time in 80 months—and that includes pandemic figures. To no surprise, hard goods are challenged. (We have explained in past notes that consumers shifted spend to services).

For Mar, what worked in the US? Quality (+4.7%) and Low Vol (+5.6%) as portfolios de-risked during the banking crisis. Growth also had its day up +4%. Value (-7.4%) and Size (-5.6%) were relative and absolute losers. Of course these moves were even more extreme in small cap value indexes. Finally, equities started to mirror the economy, with ISM-sensitive stocks underperforming. In the EZ, Quality also worked (+9.2%), which ASR says was one of the biggest moves of the last 30 years, and Low Vol also worked (+8.3%). Value managers saw a reversal after a strong 2022, with EZ Value down -6.2%. So, it’s going to be hard to stick with the same playbook for Quality given its run-up. To achieve alpha, investors may have to ding Quality a little bit (Middling Quality?) and try to find some value, a sentiment shared with ASR.

ernstein is out with a great research piece on luxury retail, calling out direct retail as the winning strategy in the space. From amazing flagship stores to online brand leadership, the mega-brands are pulling away even further from their competitors. They’re showing better retail space productivity and LFL sales growth in an economic period when fixed cost increases are the reality. Moreover, luxury brands are winning in the retail travel space for duty-free sales. So, bigger luxury brands like Gucci are having an easier time than smaller ones like Burberry.

GS is calling the upcoming earnings season as the “trough in S&P 500 earnings growth.” Consensus is for S&P EPS to be down -7% y/y. With a credit crunch still ahead of us, and reduced spend after people lose their jobs, it seems a bit premature to be “calling bottom,” but let’s hope they’re right.

NOSO put out some stats that should excite bond bulls. The UST 10-yr yield has declined for 6 days through yesterday’s close. Over the past decade, NOSO states that it’s happened 25 times, and in 17 of those cases, the 10-year yield was down ~13 bps over the next 20 days.

The Caixin China Services PMI increased to 57.8 in March, the highest level since Nov 2020.

They were hired by the US gov to sell $14bn in securities held by failed banks Signature and SVB. Most are agency mortgage-backed securities, CMOs and commercial MBS.

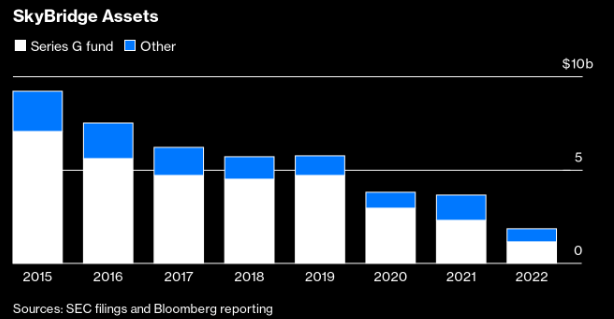

BBG is out with a story about the Mooch’s Skybridge decline, stating that clients from Morgan Stanley account for $800mm of the $1.1bn flagship fund that has done everything possible to keep investors from getting their money out. To recall, the fund made a big crypto play the past few years which came crashing down in 2022, alongside most risk assets. Anyone else wonder how this guy’s firm survives the partnership with SBF/FTX and still has $2bn in AUM?