Headlines are about Disney+ losing 4mm subscribers, mostly from India, in 1Q23. In the US and Canada, it lost 600k. Its total (157.8mm) compares to that of Netflix (232.5mm). To stem the content war losses, Disney is going to produce less content, raise prices for ad-less content—and probably lose more subscribers or at least dampen growth. After shutting down its metaverse initiatives, most likely the company will refocus on gaming. And integrating Hulu into its offering, so probably buying 100% of that.

Headlines are about Disney+ losing 4mm subscribers, mostly from India, in 1Q23. In the US and Canada, it lost 600k. Its total (157.8mm) compares to that of Netflix (232.5mm). To stem the content war losses, Disney is going to produce less content, raise prices for ad-less content—and probably lose more subscribers or at least dampen growth. After shutting down its metaverse initiatives, most likely the company will refocus on gaming. And integrating Hulu into its offering, so probably buying 100% of that.

We saw a cooling jobs market with price inflation via prints today. US initial jobless claims reached the highest level since Oct 2021. Producer prices rose 0.2% in April, just shy of the 0.3% expectation. So safe havens are up (USD, bonds).

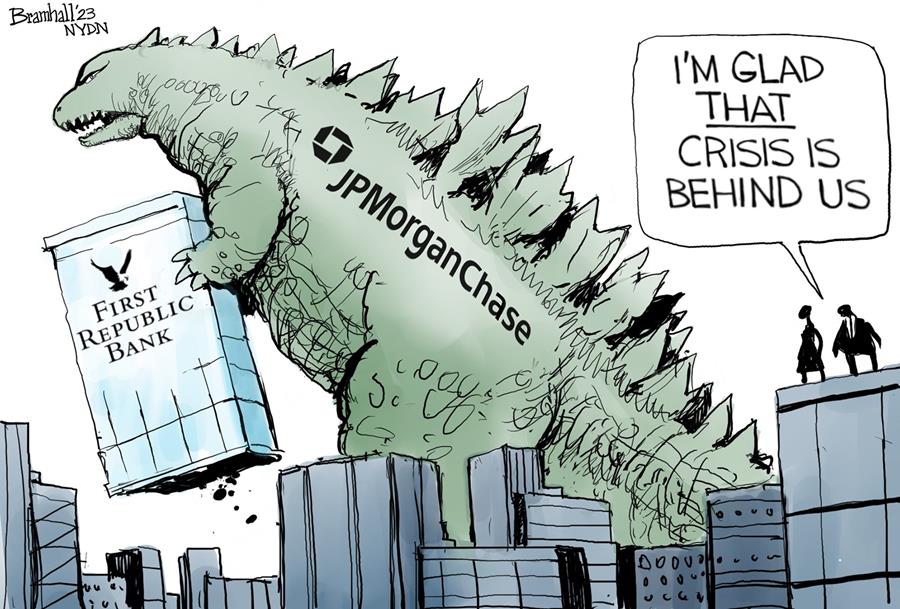

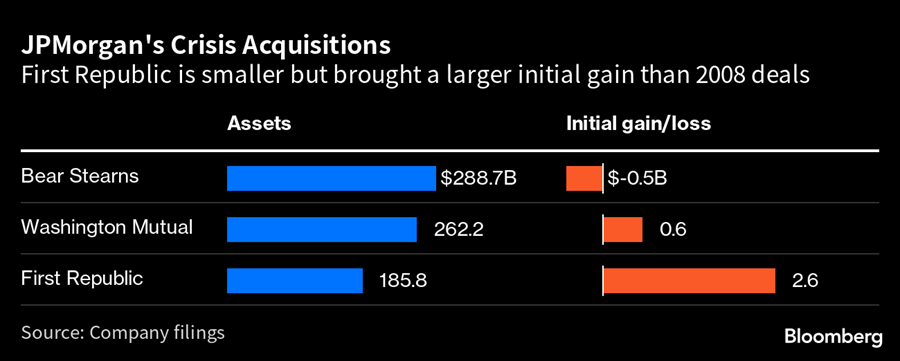

Jamie Dimon noted that there is going to be greater oversight (regulations, rules, requirements) for banks, and US regulators will probably “overdo it.” Given that third parties, including the US government, have had to quickly problem-solve to endeavor to stem a full on banking crisis because of bank mismanagement, the level of changes may or may not constitute overdoing it. Perhaps his statement was to ward off analysts who note that his shop has been a huge beneficiary of financial crises in the past.

Not to be outdone by JPM, Blackstone is talking to regional lenders. They are looking to be a middle-man. The banks would make loans. Blackstone would sell them to insurers, who would hold them to maturity. Insurers would pay Blackstone a fee.

Its stock is down again today (~-20%) because its deposits declined -9.5% last week.

That’s what the BOE did today at 25bps to 4.5%. Interestingly, the UK’s central bank says they don’t see a recession on the horizon. Lower energy prices and a fiscal spend in the spring budget are driving that call. Also, they don’t think there will be much credit tightening. But because inflation is high and sticky, they are keeping a hawkish tone, in case the lagged effects of prior tightening don’t bring it down.

If the debt ceiling is lifted, analysts expect more Treasury supply to come in at the 3-9 month tenure. That would steepen the OIS curve short-term, which would feel like a 25 bps hike as the swap curve corrects toward Treasury rate levels. T-bills maturing in the next month are priced higher than the OIS curve, compared to longer maturity ones yielding ~5.4% annualized. So money market fund managers have to decide whether to sacrifice yield for safety, or to risk a default for the higher yielding ones. If we get resolution by the June x-date, we’ll see a lot more Treasuries come to market with yields closer to the Fed Funds rate. Compared to the just-higher yields available now, the extra 0.3% doesn’t sound too exciting. But if the debt ceiling impasse continues, the Treasury could default on its coupon payments, and then investors could try to redeem their cash invested in money markets, because they don’t want a liquidity problem. So, Bloomberg is cautioning folks to stay liquid and wait.

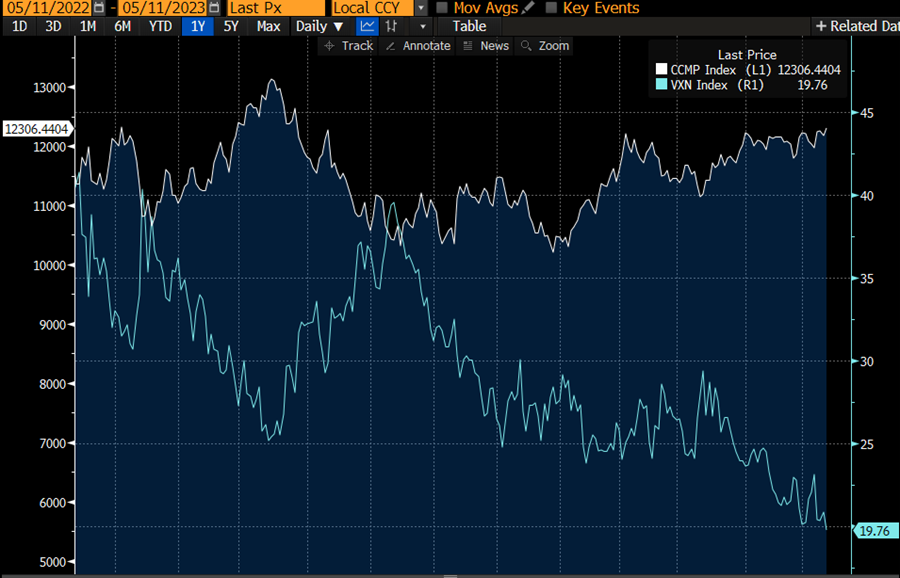

Tech is up (a lot, shown below in white for the past year). The volatility of tech is down a lot, shown in light blue. So, if you’re looking to hedge, seems like a good time because if there is any flight of capital, you know where it’s coming from. We saw the VIX pop from the 15’s just recently when everyone was calling for smooth sailing. NASDAQ broke above the resistance yesterday. Volumes remain light, and such technicals force some folks to chase returns where they’re at….until they don’t. Meta +94%, Apple +31%, Nvidia +98%, Google +27%. Right now, the number of advancing issues of the S&P only roughly equaled that for decliners. A sharp drop in rates yesterday gave BigTech a BigBoost, to hint at the handiwork of quantitatively driven strategies. Such buys tend not to be sustainable and are usually agnostic to the market’s direction.

SoftBank’s Vision Fund is still showing terrible returns, per its earnings presentation.