That’s what we’ve got this morning, with McCarthy telling the world that he doesn’t think the US will default. Biden is postponing the start of his trip, and hopefully everyone is sufficiently caffeinated to take this down the stretch.

That’s what we’ve got this morning, with McCarthy telling the world that he doesn’t think the US will default. Biden is postponing the start of his trip, and hopefully everyone is sufficiently caffeinated to take this down the stretch.

RBC coined the current market action as the “Paddling Duck Market” whereby everything looks cool on the surface, but underneath there’s a lot of activity signaling risk: concentrated returns in tech, increased hedges around the debt ceiling.

Target beat on earnings, but it wasn’t due to the topline. The co’s sales were roughly flat y/y, with consumers buying only necessities. It guided to a low-single digit decrease in sales for this quarter as well but held onto its full year guidance. Mgmt said that shoppers spent less as the quarter went on. Beauty was strongest, followed by food and beverage as well as health + pet. The stinkers were apparel and home. Moreover, digital sales were pressured. Makes sense. If people are ordering more groceries, they’ll do curbside or go in the store.

Versus Target, TJX boosted guidance for the year, even with slightly lower top line forecasts. So, consumers are trading down, and prices are staying high. We’ve written how that game only lasts for so long.

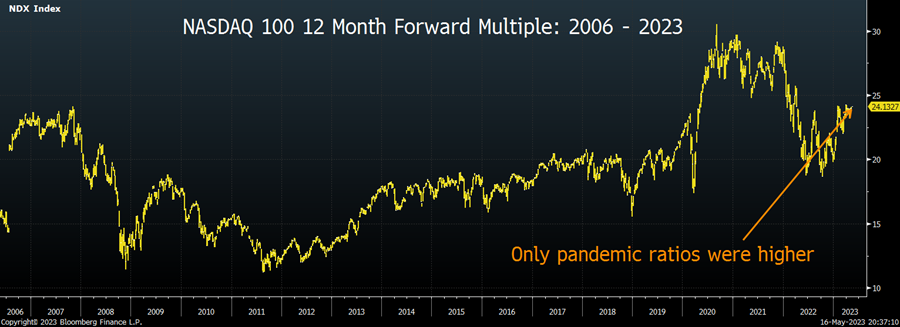

42Macro is out with a note saying that its Crowding Model is generating a bearish signal in Tech $XLK versus a bullish signal in Utilities $XLU. This jives with its Dispersion Model that is generating a GTFO Signal because of pod shop crowding into Defensive sectors and style factors. The NASDAQ 100’s forward multiple is 24.1x, above the post-Dot Com era until the pandemic. UBS provided the nice chart below:

We’ve seen the S&P trading between 3810 and 4195. The Russell between 1700 and 1800.

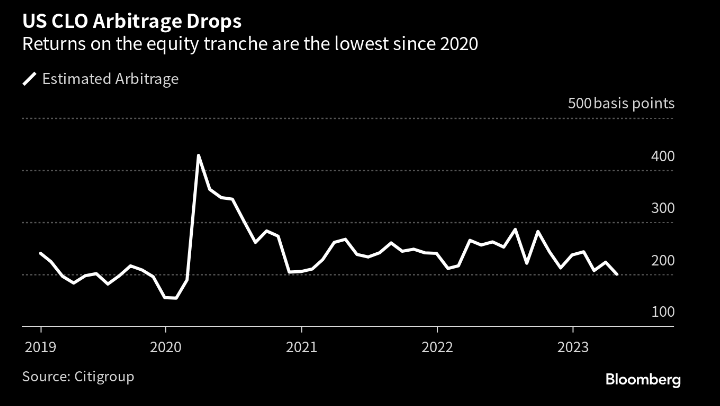

BBG is out with a piece this morning citing CLOs delivering the worst returns in years. The $1.3 trillion (with a T) market for reselling leveraged loans is in tough shape, making it more difficult for lower-rated companies to refinance their debt. The CLO market (which buys leverage loans) is in a pinch because the returns on investments are lower than the funding costs. So, folks don’t want to issue new CLOs. The spread between the yields on the loans and the yields on the repackaged CLOs is only at 200bps, per Citi. Last year the delta was 260. The lack of loan supply is increasing loan prices in the secondary market, so some folks are not buying the equity portion of the CLO structure, which is the more junior, risky part.

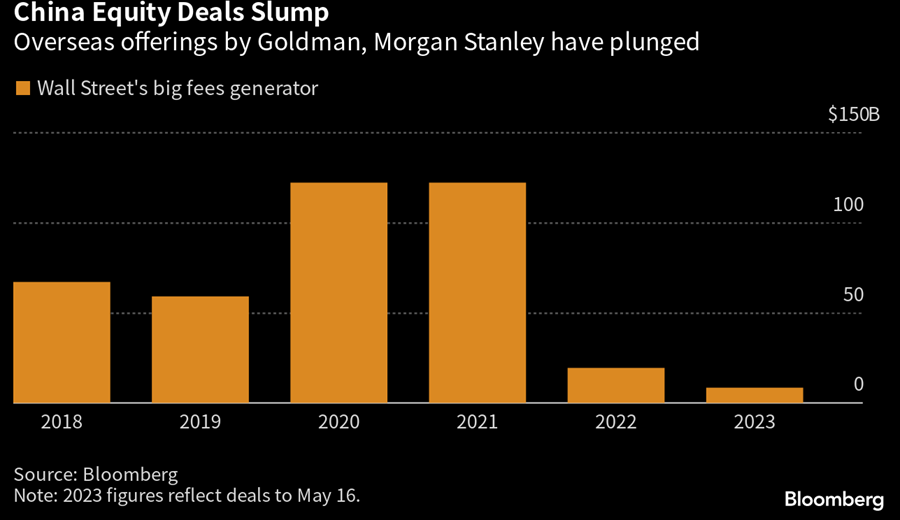

Banks like GS and Morgan Stanley are curtailing their banking ops in China because of the deteriorated business environment. They’re finding out that political actions could be too risky of a bet, and they are making the biggest cuts in years in China versus reductions in the ROW. But they still have a ton of exposure, per BBG. While it’s a huge market, it tends to be dominated by Chinese banks. You can see below how deals have taken a hit.

UBS is estimating a $35bn gain from its takeover of CS, but it does expect ~$4bn in expenses from legal and regulatory challenges.