$MSFT is up 8% after posting solid cloud reacceleration at Azure and good results across the board (LinkedIn, gaming, software, etc). Plus, they are actively touting AI, which we know is the buzzword of this decade. One wrinkle is how to deal with the UK’s opposition of the Activision deal. $GOOG also eased fears after posting a disciplined quarter that also included cloud strength, decent ads, better Youtube, a major buyback, and expense reduction plans (gotta leverage those staplers). Both companies also mentioned that they run on H-100 Nvidia graphics cards for their AI. We’ll see if $META can stay in the cool kids club and post a positive result after the market close today. Now they’ll also have to answer questions about last weekend’s ad glitch that burned their clients money. Then, we’ve got to navigate $AMZN tomorrow and $AAPL next week.

$MSFT is up 8% after posting solid cloud reacceleration at Azure and good results across the board (LinkedIn, gaming, software, etc). Plus, they are actively touting AI, which we know is the buzzword of this decade. One wrinkle is how to deal with the UK’s opposition of the Activision deal. $GOOG also eased fears after posting a disciplined quarter that also included cloud strength, decent ads, better Youtube, a major buyback, and expense reduction plans (gotta leverage those staplers). Both companies also mentioned that they run on H-100 Nvidia graphics cards for their AI. We’ll see if $META can stay in the cool kids club and post a positive result after the market close today. Now they’ll also have to answer questions about last weekend’s ad glitch that burned their clients money. Then, we’ve got to navigate $AMZN tomorrow and $AAPL next week.

Analysts are upgrading Chipotle $CMG after a big EPS beat, given lower food costs to higher prices to improved throughput.

Mortgage applications to buy a home were up +5% w/w, and refi applications were up +2% w/w. The ave interest rate for a 30-year fixed mortgage is at 6.55%. With home prices a bit lower, folks must be doing the math and executing.

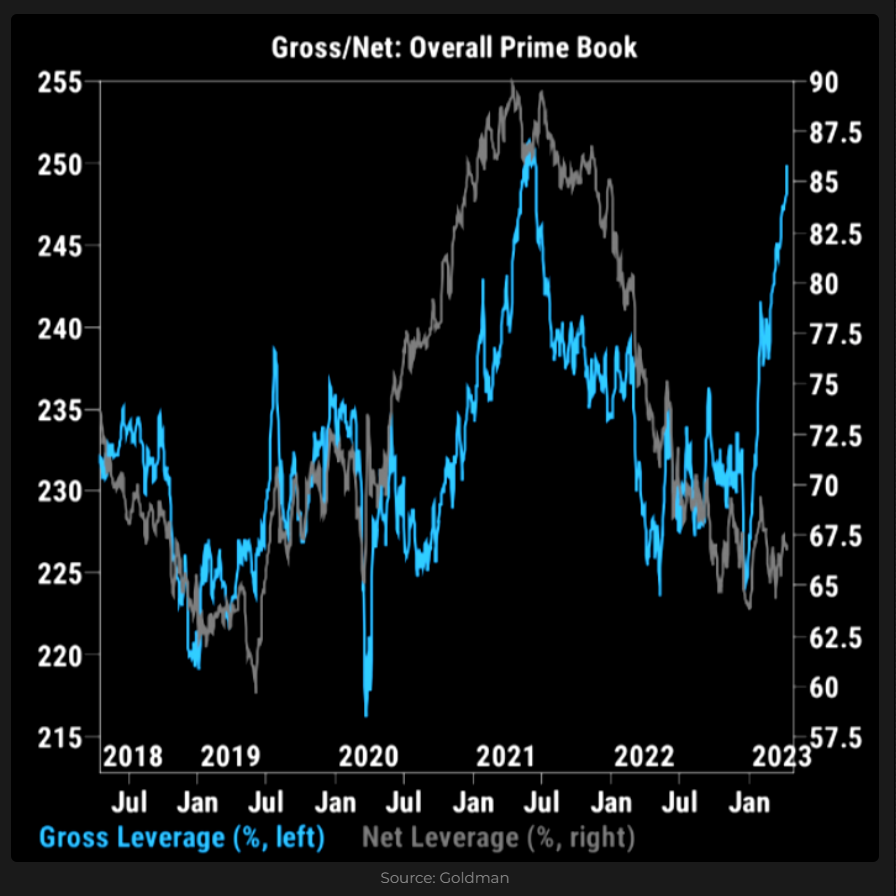

Goldman is raising the caution flag on quants being “out of ammo,” as systematic managers increased global positions by more than $170bn in the last month, bringing their exposure to the highest since early 2022. If the market declined, Goldman estimates that they’d have to unwind closer to $276bn, so that’s a lot of downside asymmetry. Per the chart (below) from Goldman, gross exposures are at major highs.

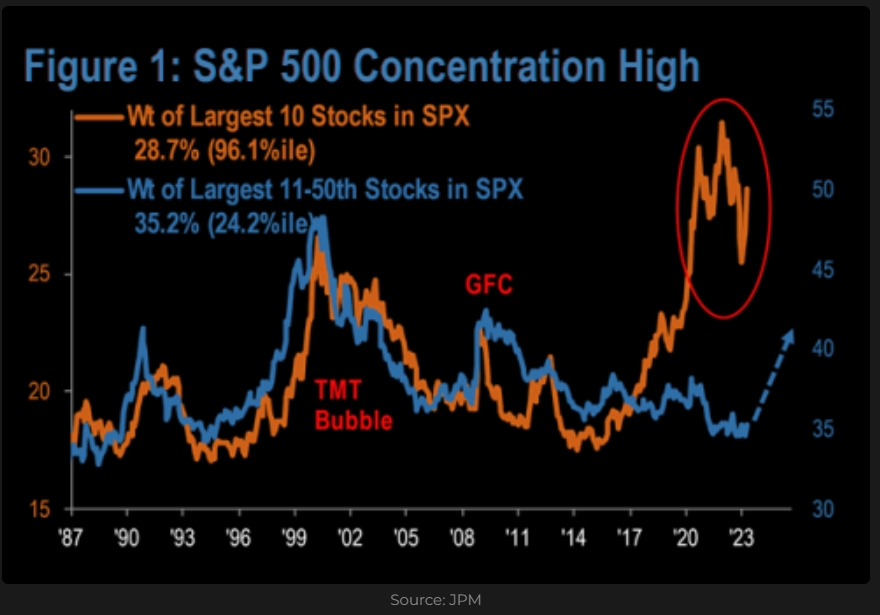

There’s too many people in the same names. The top 10 stocks’ market caps are at their 96th percentile relative to S&P history, per BTIG. The weight of the largest 2 stocks in the S&P are at new highs. Six companies (MSFT, GOOGL, AMZN, META, NVDA, CRM) drove 53% of the S&P’s performance, 54% of NASDAQ’s performance, and 68% of the Growth factor’s performance (per JPM).

That’s the question for the ECB on raising rates. Inflation is too high. Riksbank just did another 50bps hike and forecasted another 25bps coming down the pike.

WTI edged back up after the API report. Gold is firm after 2 days of strength. Wheat is down given a Canadian strike.

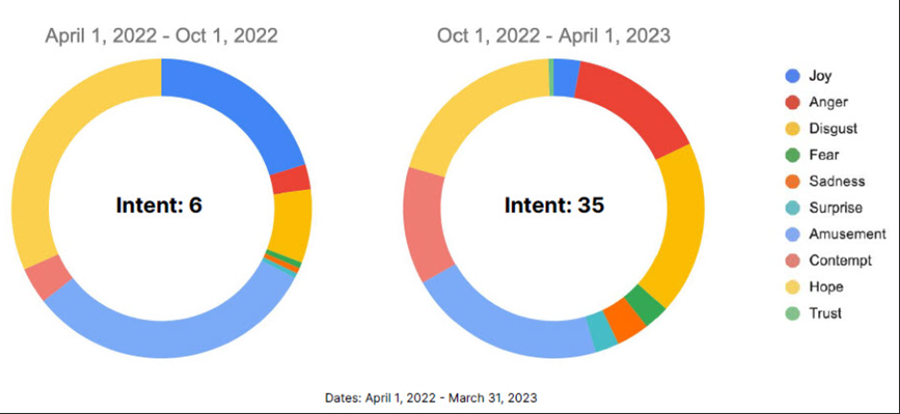

at combo doesn’t usually work with consumers for too long. $SBUX customers are getting madder about price hikes, per Cognovi Labs, and are weighing their options (fewer visits, making coffee at home, halting food purchases, trading down, and completely avoiding the nasty sounding olive oil drink). Customers are feeling a lot more anger and contempt for the brand. The data compares to that for McD’s, where customers have become apathetic about their price increases, because of the total dollar value of purchases.