It’s all about Powell’s Q&A today and forecasted dissent within the ranks. 2pm ET report. 2:30pm ET Q&A. He’s got his work cut out for him. ADP April data showed strong jobs data versus forecasted. But banks are failing. Fight inflation? Or reduce pressure on the financial system?

It’s all about Powell’s Q&A today and forecasted dissent within the ranks. 2pm ET report. 2:30pm ET Q&A. He’s got his work cut out for him. ADP April data showed strong jobs data versus forecasted. But banks are failing. Fight inflation? Or reduce pressure on the financial system?

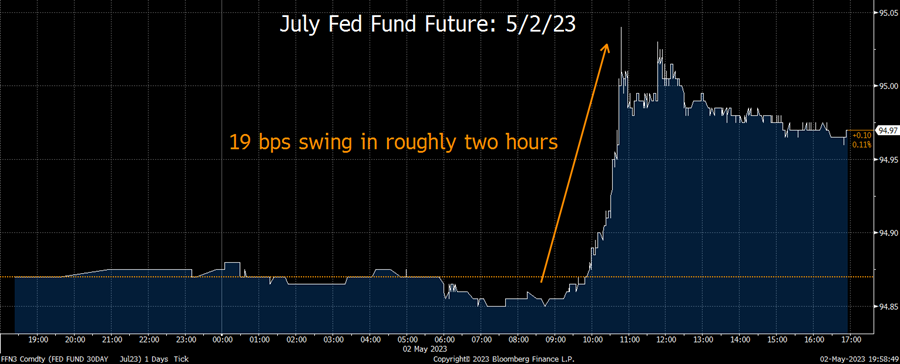

Yesterday, before the market opened, the July Fed Fund future implied that traders had a 28% bet that Powell would increase overnight rates by 25bps in June. Before mid-day, traders had shifted its view to a 46% probability that the Fed would cut rates by 25bps by June. So, if you think there is a strong, consistent consensus out there, well, there’s not. Pick your day and hour. Check out this chart per UBS/Bloomberg:

Yep, it was up again yesterday. Seems like folks are concerned about a recession and credit crunch, and the move also probably reflected a trade toward safety as Treasury yields dropped.

Estee Lauder is down hard this morning. Management cited pressures in Asia travel retail and forecasted even more headwinds in the next quarter. Management pointed to volatile and gradual reopening spend in Asia.

It’s below $70. This week both BP and Shell were down hard. Investors were upset with BP’s projected lower 2023 surplus cash generation ($36bn versus $50bn last year), which would translate into lower buybacks than hoped this year. BP is reducing debt, staying disciplined on capital, and returning around $8b+ to shareholders via buybacks (versus around $10bn expected), with a gradual dividend recovery, lowering BP’s distribution yield to around 12%.

Eli Lilly is up after positive results in a final-stage trial of its Alzheimer’s drug. I know that many families are hopeful that there will be more, successful options for loved ones.

GS is noting that 75% of the S&P will be out of their buyback periods by the end of the week, which could provide some upside pressure on stocks.

We’re hearing that folks were very active yesterday. Hedge funds were balanced with buys/sells yet with below ave shorting into Fed day. International flows were buying. Mutual funds were buying. Areas for buys? Healthcare, mining, ecommerce, financials and utes/reits. Most sells in MLPs. Both tech and energy had balanced 2-way flows.

That’s what hurting Starbucks today. They kept guidance for the year after posting a strong quarter. So, investors are either calling the guidance conservative or a forecast for projected slowdown. With a new CEO on board, it’s probably a little bit of both. Same store sales were +11%. China also improved faster than expected.

That’s the time that the SEC would give big hedge funds (>$1.5bn AUM) to disclose big losses or margin events. Folks expect this to be adopted today. Historically, the period to report was quarterly. Private equity firms also would have new reporting requirements (GPs leaving, fund terminations, leverage use, compensation). Moreover, the SEC is also looking at rules to force public companies to disclose more info about their share repurchases, so investors could figure out if they are timed to benefit executives or shareholders.